FINANCIAL-ACCOUNTING-AND-REPORTING Online Practice Questions and Answers

Questions 4

An extraordinary gain should be reported as a direct increase to which of the following?

A. Net income.

B. Comprehensive income.

C. Income from continuing operations, net of tax.

D. Income from discontinued operations, net of tax.

Questions 5

During 1994, Orca Corp. decided to change from the FIFO method of inventory valuation to the weightedaverage method. Inventory balances under each method were as follows:

Orca's income tax rate is 30%.

Orca should report the cumulative effect of this accounting change as a(n):

A. Adjustment to beginning retained earnings.

B. Component of income from continuing operations.

C. Extraordinary item.

D. Component of income after extraordinary items.

Questions 6

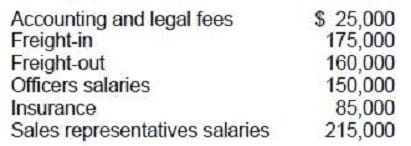

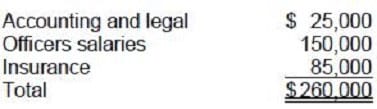

The following costs were incurred by Griff Co., a manufacturer, during 1992:

What amount of these costs should be reported as general and administrative expenses for 1992?

A. $260,000

B. $550,000

C. $635,000

D. $810,000

Questions 7

In which of the following situations should a company report a prior-period adjustment?

A. A change in the estimated useful lives of fixed assets purchased in prior years.

B. The correction of a mathematical error in the calculation of prior years' depreciation.

C. A switch from the straight-line to double-declining balance method of depreciation.

D. The scrapping of an asset prior to the end of its expected useful life.

Questions 8

Rock Co.'s financial statements had the following balances at December 31:

What amount should Rock report as comprehensive income for the year ended December 31?

A. $400,000

B. $420,000

C. $520,000

D. $570,000

Questions 9

Which of the following is correct concerning financial statement disclosure of accounting policies?

A. Disclosures should be limited to principles and methods peculiar to the industry in which the company operates.

B. Disclosure of accounting policies is an integral part of the financial statements.

C. The format and location of accounting policy disclosures are fixed by generally accepted accounting principles.

D. Disclosures should duplicate details disclosed elsewhere in the financial statements.

Questions 10

A change from the cost approach to the market approach of measuring fair value is considered to be what type of accounting change?

A. Change in accounting estimate.

B. Change in accounting principle.

C. Change in valuation technique.

D. Error correction.

Questions 11

According to the FASB conceptual framework, predictive value is an ingredient of:

A. Option A

B. Option B

C. Option C

D. Option D

Questions 12

The following items were among those that were reported on Lee Co.'s income statement for the year ended December 31, 1989:

The office space is used equally by Lee's sales and accounting departments. What amount of the abovelisted items should be classified as general and administrative expenses in Lee's multiple-step income statement?

A. $290,000

B. $325,000

C. $410,000

D. $500,000

Questions 13

On January 2, 1993, Quo, Inc. hired Reed to be its controller. During the year, Reed, working closely with Quo's president and outside accountants, made changes in accounting policies, corrected several errors dating from 1992 and before, and instituted new accounting policies. Quo's 1993 financial statements will be presented in comparative form with its 1992 financial statements. This question represents one of Quo's transactions. List A represents possible clarifications of these transactions as: a change in accounting principle, a change in accounting estimate, a correction of an error in previously presented financial statements, or neither an accounting change nor an accounting error.

Item to Be Answered During 1993, Quo determined that an insurance premium paid and entirely expensed in 1992 was for the period January 1, 1992, through January 1, 1994.

List A (Select one)

A. Change in accounting principal.

B. Change in accounting estimate.

C. Correction of an error in previously presented financial statements.

D. Neither an accounting change nor an accounting error.

![]()

![]()

Home | About Us | Contact Us | FAQ | Guarantee Policy | Privacy Policy

Any charges made through this site will appear as Global Simulators Limited. All trademarks are the property of their respective owners.

Copyright © 2004-2026 pass2lead.com, All Rights Reserved.